A very American dispute. The issue of AM radio in vehicles sold in the USA has been debated for many years, but electrical vehicles (EVs)bring this issue to a head...

Inventory correction is in full swing. Weak numbers from Texas Instruments echo what Mobileye highlighted a few weeks ago underlining that industrial semiconductors are now enduring the same correction that...

Slowdown actually helps OEMs. The realities of electric vehicles are starting to come home as the early adopters now all have an EV while the rest of us are...

Life in autonomy remains dreadful. There is little hope for a recovery in autonomous driving anytime soon as programs are being cancelled meaning that my 2028 target looks increasingly over...

There was very wow this year as I had already seen almost every product that was on display but critically, these products were closer to market than they were last...

CES comes to life. After a quiet start on Tuesday, CES 2024 came back to life on Wednesday with a substantial increase in footfall, crowds and queues. This is an...

AI delivery – Time to deliver. 2023 was dominated by hype, speculation and spending on AI training infrastructure but 2024 is where the rubber will likely meet the road. Already...

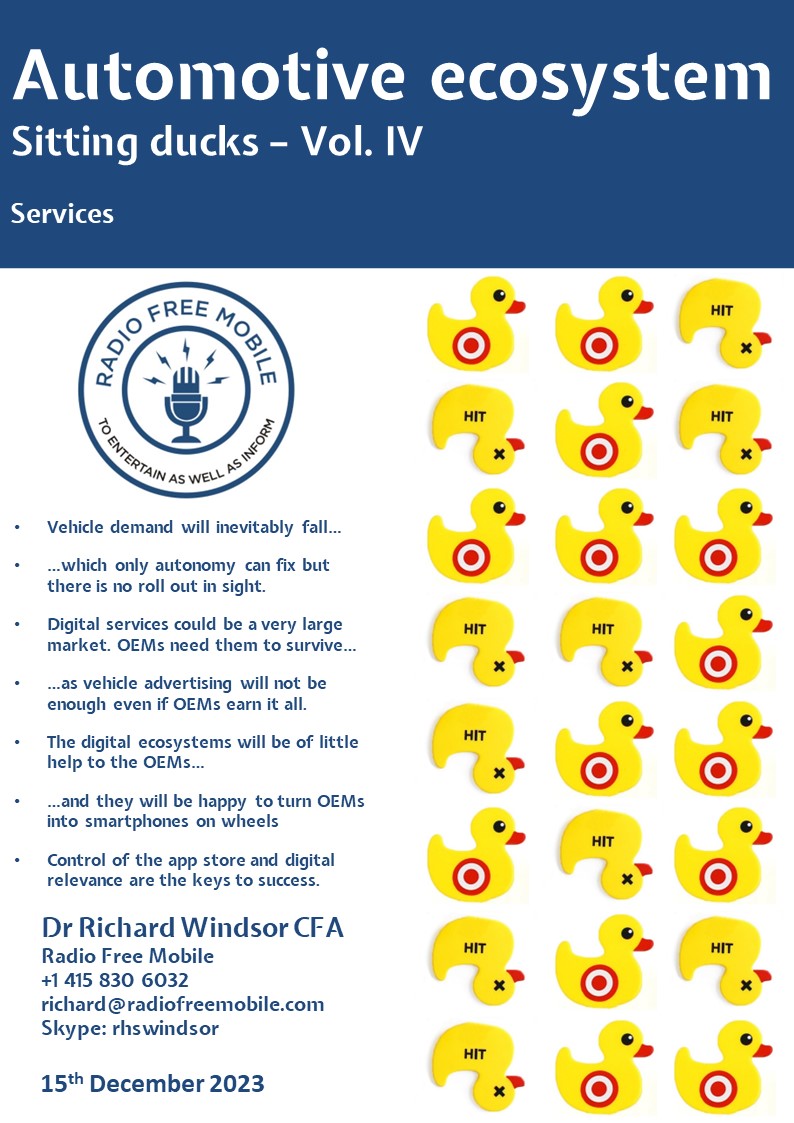

15th December 2023 – Radio Free Mobile extends its coverage of the automotive digital ecosystem with the publication of Automotive Ecosystem – Sitting Ducks Vol. IV – Services. RFM research...

Autonomous driving plumbs new depths Tesla’s recall takes autonomous driving to a new level of doubt and depression, but it is precisely at the point at which everyone is about...

Richard is founder, owner of research company, Radio Free Mobile. He has 16 years of experience working in sell side equity research. During his 11 year tenure at Nomura Securities, he focused on the equity coverage of the Global Technology sector.

Qualcomm FQ1 24 – On the up

Apple remains toothless. Good results combined with further confirmation that Apple is in no position to restart its patent fight with Qualcomm, result in a company with good short and...